Mortgage in Poland for Foreigners: Complete Guide 2025

Poland is becoming an increasingly popular destination for property purchases by foreigners. However, obtaining a mortgage in Poland for non-residents has its specific features that need to be considered. Let’s examine who among foreigners is eligible for a mortgage, what are the conditions for obtaining it, what documents need to be provided, and what is the procedure for getting a mortgage loan.

Who is Eligible for a Mortgage in Poland?

The right to obtain a mortgage loan in Poland is available not only to Polish citizens but also to foreigners who meet certain criteria. The key factor is proving stable and sufficient income to cover monthly loan payments. Banks also pay attention to:

Basic Requirements for Foreign Borrowers

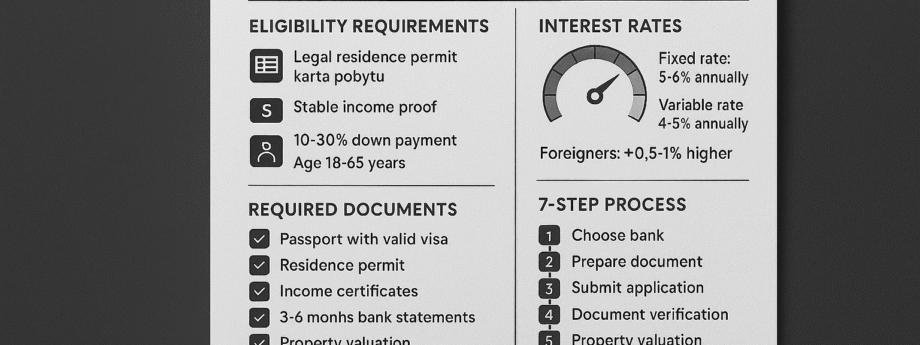

- Legal residence in Poland. Usually, a residence permit (karta pobytu) or other legal basis for long-term residence is required. A temporary visa is typically insufficient. Residence duration requirements vary depending on the bank and lending program.

- Credit history. While having a credit history in Poland is an advantage, some banks are willing to consider applications from foreigners with a positive credit history in their country of origin.

- Purpose of the loan. The loan must be intended for purchasing property in Poland.

- Down payment: As in most countries, banks require a down payment, usually ranging from 10% to 30% of the property value.

Mortgage Conditions for Foreigners in Poland

The conditions for obtaining a mortgage for foreigners may be stricter than for Polish citizens. Banks most often require the following from non-residents:

1. Legal Residence Documentation

The main requirement of virtually all banks is having a document confirming legal residence in Poland. This can be:

- Temporary residence card (Karta czasowego pobytu), issued for up to 3 years

- Permanent residence card (Karta stałego pobytu), providing indefinite residence rights but requiring renewal every 10 years

When concluding a mortgage, banks prefer clients with long-term residence permits.

2. Proof of Stable Income

The second important condition is proof of stable income for foreign citizens, sufficient to service the loan. This document would be an income certificate for the last 3-6 months. Income can also be confirmed through:

Types of Income Verification:

- Employment contract (Umowa o pracę). In this case, banks prefer candidates with indefinite-term contracts.

- Civil law contracts (Umowa zlecenie, Umowa o dzieło). Not every bank is willing to accept them due to their temporary nature.

- Own business. Income from business activities can also be accepted by the bank. However, the business must have been operating for at least 12-24 months and have no tax debts.

3. Additional Conditions for Foreigners

- Higher down payment – due to increased risks associated with non-residents, the bank may request a larger down payment.

- Higher interest rate. The interest rate may be 0.5-1% higher than for Polish citizens.

- Additional guarantees. The bank may require additional guarantees, such as a guarantee from a Polish resident or collateral on other property.

- More thorough document verification. The process of verifying documents and financial status may take longer.

4. Loan Amount Calculation

The mortgage loan amount depends on two factors – your creditworthiness and the property value. The bank assesses your creditworthiness based on your monthly net income and expenses, as well as the number of dependents.

Approximately, the bank can provide a loan of PLN 100,000 for every PLN 1,500 of your net monthly income. However, each dependent (spouse, children) reduces this amount by PLN 100,000.

5. Age and Loan Currency

- Borrower’s age. Loans are available to people aged 18 to 60-65 – i.e., working age.

- Loan currency. According to the rules of the Polish Financial Supervision Authority (Komisja Nadzoru Finansowego), the loan currency in Poland must match the borrower’s income currency.

Required Documents

The list of documents for a mortgage may vary depending on the bank, but usually includes:

Basic Document Package:

- Loan application – a completed form with personal data, income, and expenses.

- Passport or other identity document with a valid visa or residence permit.

- Documents confirming legal residence in Poland – residence permit, work permit, etc.

- Income verification documents – income certificates from the workplace, tax declarations.

- Bank account statement confirming funds for the down payment.

- Property purchase agreement or preliminary agreement.

- Property valuation. Independent valuation of the purchased property.

- Credit history (if available) from the country of origin or Poland.

Mortgage Application Process

Step-by-Step Instructions:

- Choose a bank. Compare offers from different banks and choose the most suitable option.

- Document preparation. Gather all necessary documents.

- Submit application for a loan at the chosen bank.

- Document verification and risk assessment. The bank verifies the provided documents and assesses the applicant’s creditworthiness.

- Property valuation. An independent property valuation is conducted.

- Loan approval. If the bank approves the application, the loan agreement is signed.

- Loan disbursement. Loan disbursement after completion of the property purchase transaction.

Loan Amount and Interest Rates

The approved loan amount directly depends on the appraised property value, which is often lower than the market value. Therefore, don’t expect the full amount – 70-80% of the market value declared by the bank may be significantly less than expected.

Types of Interest Rates

The choice of rate type also affects the loan amount. Fixed rate (usually for 5-10 years) and long-term loans increase risks for the bank, which may reduce the maximum possible loan amount. Variable rate, in turn, is subject to changes depending on market conditions.

As of November 2024, average mortgage interest rates in Poland are:

- 5-6% annually for fixed rates

- 4-5% annually for variable rates

- For foreign citizens, interest rates may be 0.5-1% higher

Insurance

Obtaining a mortgage loan often involves mandatory insurance for both the borrower and the purchased property.

Types of Mortgage Insurance

Property Insurance

Property insurance protects against damage caused by destruction or natural disasters (fire, flood, earthquake), usually for the loan amount or market value of the property.

Borrower’s Life Insurance

Borrower’s life insurance is especially important for long-term mortgages or large loan amounts. In case of the borrower’s death or disability, insurance guarantees either loan repayment by the bank or transfers payment responsibility to guarantors.

Insurance Costs

- Property insurance in Poland costs 0.03-0.1% of the property value per year (e.g., for an apartment worth PLN 400,000 – PLN 120-400 per year).

- Life insurance cost depends on the borrower’s age, health, and loan amount, ranging from 0.02-0.05% of the loan amount per month.

Costs Associated with Mortgage Loan in Poland

Let’s examine what mortgage-related costs the borrower should be prepared for:

Main Cost Items:

- Down payment – banks usually require the borrower to pay 10-20% of the property value, however, for foreigners, the percentage may be higher.

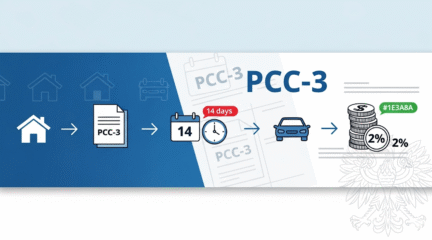

- Tax on civil law transactions (PCC). For secondary market purchases, the rate is 2% of the property value.

- VAT on the primary market. VAT rates for residential property:

- 8% – for apartments up to 150 m² and houses up to 300 m²

- 23% – for properties exceeding these limits

- Property valuation. Appraiser services cost approximately PLN 300-700.

- Notarial services. Notarial fees can range from PLN 1,000 to 3,000.

- Bank commission for mortgage processing – from 0 to 2% of the loan amount.

- Land registry registration (Księga Wieczysta). Mortgage registration costs PLN 200.

- Other costs:

- Legal services: PLN 200-2,000

- Real estate agency services: 2-5% of the property value

Property Purchase Process in Poland: Main Stages

If you’ve decided to purchase property in Poland, let’s look at the main stages you’ll need to go through:

Property Purchase Stages:

- Property selection and document verification. At this stage, it’s important to check all documents related to the property, including ownership rights, plans, mortgages (if any).

- Signing a preliminary purchase agreement (umowa przedwstępna). This agreement establishes the intention to buy the property and usually includes a deposit.

- Payment. Payment is usually made after checking all documents and signing the preliminary agreement.

- Notarial deed (akt notarialny). This is the final stage where the deed is signed at the notary’s office. After signing the notarial deed, you become the legal owner of the property.

- Payment of taxes and fees. When purchasing property, you need to pay the PCC tax (2% of the property value).

Who Can Help with Property Purchase in Poland

Specialists for Consultation:

- Notary in Poland. The notary is a key figure in the property purchase process. They will verify all documents, ensure the legality of the transaction, and prepare the ownership transfer deed.

- Polish lawyer. A lawyer can help you understand the legal aspects of the transaction, verify documents, and protect your interests.

- Real estate agencies in Poland. Real estate agents can help you find suitable property and guide you through the purchase process.

IMPORTANT! It’s essential to know that for a successful transaction, it’s crucial to consult professional and verified lawyers and notaries who will help you go through all necessary stages and avoid potential problems. Independent purchase without professional help can be risky.

Conclusion

Obtaining a mortgage in Poland for foreigners is possible but requires careful preparation and meeting certain conditions. It’s important to familiarize yourself with the requirements in advance. Purchasing property in Poland with a mortgage can also be an excellent investment opportunity.

If you have any questions, please contact us at office@progressholding.pl

Split payment in Poland — when it’s mandatory and how it affects your cash flow

Split payment in Poland — when it’s mandatory and how it affects your cash flow

Shareholder loans in Poland: when is PCC tax due and when is it exempt?

Shareholder loans in Poland: when is PCC tax due and when is it exempt?

PCC-3 tax Poland 2025 – how to file declaration

PCC-3 tax Poland 2025 – how to file declaration

How to open a corporate bank account in Poland in 2026 as a foreigner?

How to open a corporate bank account in Poland in 2026 as a foreigner?

Property rental taxation in a Polish LLC (sp. z o.o.) — CIT, VAT, and depreciation

Property rental taxation in a Polish LLC (sp. z o.o.) — CIT, VAT, and depreciation

Tax Return in Poland and Tax Refund Guide 2025 – Complete Instructions for Individuals and Companies

Tax Return in Poland and Tax Refund Guide 2025 – Complete Instructions for Individuals and Companies

View also

Thursday April 30th, 2026

The office will be closed on May 1, 2026

Wednesday April 29th, 2026

Selling shares in a Polish LLC to a foreigner — procedure, taxes, and corporate approvals

Tuesday April 28th, 2026