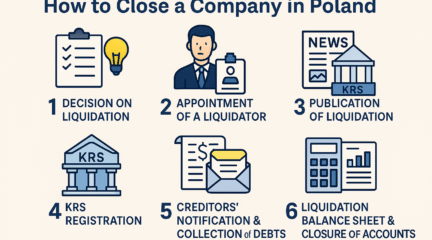

Closing a limited liability company (Sp. z o.o.) in Poland in 2026 requires a formal liquidation process. You must pass a shareholders’ resolution, appoint a liquidator, and report the opening of liquidation to the National Court Register (KRS). Next, you summon creditors in the Court and Economic Monitor, settle taxes, and submit an application to delete the company from the register.

What does the liquidation of a limited liability company in Poland involve in 2026?

Liquidation of a Sp. z o.o. is the process of ending its operations, paying off debts, and distributing the remaining assets among shareholders. The company exists until it is removed from the National Court Register (KRS).

Dissolution vs. liquidation – what is the difference?

Dissolution of the company occurs only at the moment of its removal from the KRS. Liquidation is the intermediate stage leading to this removal. During liquidation, the company still has legal personality and must settle taxes.

The company name should include the suffix “in liquidation” (w likwidacji). You see it in the KRS, e.g., “ABC Sp. z o.o. w likwidacji”. This suffix informs contractors and offices that you are closing operations.

The primary goal of company liquidation

The goal of liquidation is to organize all company affairs. You must finish current business, collect receivables, and pay off creditors. Only at the end can you divide any remaining assets among the shareholders.

If the company has debts, you pay creditors first. Shareholders receive funds only from the surplus after satisfying or securing all obligations.

What are the legal grounds for closing a limited liability company?

Liquidation of a Sp. z o.o. is primarily regulated by the Code of Commercial Companies and tax laws. The liquidation procedure is described in detail in the chapter on the dissolution and liquidation of a limited liability company.

Key regulations you must know

The legal basis is the Act of September 15, 2000 – Code of Commercial Companies, specifically Articles 270–290 regarding dissolution and liquidation. You can find the current text in the Internet System of Legal Acts (ISAP).

Tax obligations stem from the CIT Act for the company and the PIT Act for shareholders. Current versions can be found on the portal podatki.gov.pl. VAT is regulated by the provisions of the Goods and Services Tax Act.

Where to look for official information on liquidation?

A practical description of the procedure can be found on the government portal biznes.gov.pl – Dissolution and liquidation of companies entered in the KRS. There you will also find tips on documents and fees.

Information about the KRS and electronic submission of applications can be found on the Ministry of Justice website and in the Court Registers Portal PRS.

How to conduct the liquidation of a limited liability company step by step?

Standard company liquidation consists of several mandatory steps. You start with a shareholders’ resolution and end with an application to delete the company from the KRS.

Step 1 – resolution on company dissolution and opening of liquidation

Shareholders adopt a resolution on the dissolution of the company and the opening of liquidation. This usually requires the form of a notarial deed. In the same resolution, you appoint liquidators and determine the method of company representation.

Liquidators are usually the current management board members, but you can appoint other people. If you are a foreigner, you can become a liquidator as long as you meet the general requirements of Polish law. At Progress Holding, we help prepare the content of resolutions and communication with the notary.

Step 2 – suffix “in liquidation” and data update

From the moment liquidation is opened, you must use the suffix “in liquidation” (w likwidacji) in the company name. This obligation comes from the Code of Commercial Companies. This applies to stamps, invoices, correspondence, and the company website.

The change should immediately appear in documents and contracts. For contractors, this is a signal that the company is no longer entering into new contracts typical for its business but is focusing on concluding current affairs.

Step 3 – reporting the opening of liquidation to the KRS via PRS

You report the opening of liquidation to the KRS within 7 days of its commencement. The report is made by the liquidator via the Court Registers Portal PRS.

You submit the application exclusively electronically, signing it with a qualified signature, trusted profile, or e-ID card. This implements the principles described, among others, on the KRS page on gov.pl. As Progress Holding, we can prepare a complete draft of the application and attachments so that you only have to sign them.

Step 4 – announcement of liquidation in the Court and Economic Monitor

The liquidator is obliged to announce the dissolution of the company and the opening of liquidation in the Court and Economic Monitor (MSiG). In the announcement, you summon creditors to report their claims within a period of at least three months from the date of the announcement.

The obligation to summon creditors results from Art. 279 of the Code of Commercial Companies. Lack of proper announcement may block the subsequent division of assets. In practice, preparing the correct content of the announcement often requires the support of a lawyer or advisor.

Step 5 – opening balance sheet of liquidation and liquidation activities

Within 15 days of opening the liquidation, you prepare the opening balance sheet of liquidation in accordance with the Accounting Act. This balance sheet is approved by the shareholders’ meeting. Data from the balance sheet serves as a starting point for further decisions.

During liquidation, liquidators perform so-called liquidation activities. You conclude current company affairs, collect receivables, sell assets, and pay off obligations. At this stage, it is good to have an accountant who will correctly settle revenues and costs during the liquidation period – Progress Holding can take over the entire accounting service of the company in liquidation.

Step 6 – distribution of assets after liquidation

Distribution of assets among shareholders is possible only after satisfying or securing all creditors. Additionally, at least six months must pass from the announcement of the opening of liquidation and summoning creditors in the MSiG.

The six-month rule results from Art. 286 § 1 of the Code of Commercial Companies. As a rule, assets are divided in proportion to shares, unless the articles of association provide otherwise. Shareholders can receive both cash and tangible assets.

Step 7 – liquidation report and application for removal from KRS

After completing liquidation activities, the liquidators prepare a liquidation report. The report is approved by the shareholders’ meeting. The document is stored like annual financial statements.

Then the liquidator submits an application for the company’s removal from the KRS via PRS. According to information on the biznes.gov.pl portal, the application for removing an entity from the register of entrepreneurs is subject to a court fee of PLN 300. Additionally, you pay a fee for publishing the removal announcement in the MSiG.

What obligations towards KRS and MSiG do you have during company liquidation?

During company liquidation, you make several mandatory reports to the KRS and announcements in the Court and Economic Monitor. They concern both the opening of liquidation and its conclusion.

Reports to KRS – when and what do you report?

You report to the KRS primarily: opening of liquidation, appointment of liquidators and their method of representation, as well as the conclusion of liquidation and application for removing the company. You submit applications exclusively electronically via PRS.

You have 7 days to report the opening of liquidation, according to information indicated on government websites, e.g., podatki.gov.pl – business liquidation. In practice, it is worth preparing all documents earlier to avoid court summons to supplement deficiencies.

Announcements in the Court and Economic Monitor

At least two announcements in MSiG are standard when liquidating a company. The first concerns the opening of liquidation and summoning creditors, the second – the removal of the company from the KRS.

The fee for each announcement is separate. The amount of fees is determined by regulations regarding MSiG and information published by the Ministry of Justice. In practice, we prepare announcements for Progress Holding clients in full wording to meet the requirements of Art. 279 and 286 of the Code of Commercial Companies.

Obligations towards CRBR

A limited liability company is obliged to report and update information on beneficial owners in the Central Register of Beneficial Owners (CRBR). This obligation also applies to a company in liquidation.

Current information and access to the application form can be found on the Ministry of Finance website dedicated to CRBR: gov.pl – CRBR. At Progress Holding, we help determine which changes require a CRBR update and prepare the report on your behalf.

What tax and ZUS obligations arise when liquidating a limited liability company?

When liquidating a company, you must take care of tax settlements and deregister the company as a contribution payer in ZUS. There are also tax consequences for shareholders.

CIT and VAT settlements on the company side

A company in liquidation continues to submit CIT declarations and JPK_V7 files as long as it conducts taxable activities. The last tax year ends on the day liquidation is concluded, not at the end of the calendar year.

After removing the company from the KRS, a VAT-Z notification must be submitted, which serves to deregister the VAT taxpayer. The VAT-Z form template can be found in the VAT forms section on podatki.gov.pl. The Progress Holding team can prepare the final CIT, JPK, and VAT-Z declarations to close your settlements.

NIP-8 and other reports to the tax office

Changes in company data, including information on liquidation, are reported to the tax office on the NIP-8 form. The NIP-8 form is used to report supplementary data of an entity entered in the KRS.

Information about the NIP-8 form can be found in official Ministry of Finance materials, including e-forms available through the e-Deklaracje system. In practice, you will use NIP-8 both upon opening liquidation and after removing the company from the KRS.

Deregistration from ZUS as a contribution payer

If the company employed employees, you must deregister them from insurance and deregister the contribution payer. According to information on the ZUS website, in the case of companies entered in the KRS, data on the termination of operations reach ZUS based on reports to the KRS and the tax office.

Details can be found in the “Payer Deregistration – KRS companies” tab on zus.pl. As a rule, it is necessary to submit documents deregistering employees (ZUS ZWUA) and family members (ZUS ZCNA). At Progress Holding, we coordinate these reports together with HR and payroll settlements.

Tax consequences for shareholders

Assets received by shareholders after the liquidation of a limited liability company constitute income from capital gains. The surplus over expenses for taking up or acquiring shares is subject to taxation.

The legal basis consists of the provisions of the Personal Income Tax Act. In practice, each shareholder should analyze the settlement with a tax advisor, especially when receiving asset components with a difficult-to-determine market value. At Progress Holding, we prepare tax calculations for shareholders based on the company’s accounting data.

How long does it take and how much does it cost to liquidate an LLC in 2026?

Liquidation of a Sp. z o.o. usually takes from 8 to 12 months, sometimes longer. Costs consist of court fees, announcements in MSiG, and notarial, accounting, and legal fees.

Minimum duration of liquidation

The minimum liquidation time results from regulations on summoning creditors and dividing assets. The term of 3 months applies to reporting claims after the announcement in MSiG, and 6 months – the minimum period for dividing assets among shareholders.

This means that in practice, the liquidation of a limited liability company will not end sooner than a few months after the announcement in MSiG. Additionally, you must include the time for considering applications by the KRS.

Major official costs during liquidation

Official costs include the court fee for the application to remove the company from the KRS – PLN 300. This information is confirmed by the official description of the procedure on biznes.gov.pl.

Additionally, you pay fees for announcements in MSiG, including for the announcement of opening liquidation and removing the company. Added to this are the notary’s remuneration for resolutions, accounting service costs, and liquidator’s remuneration if provided for.

Table: key deadlines in the liquidation of a limited liability company

| Stage | Deadline | Basis / source |

|---|---|---|

| Reporting opening of liquidation to KRS | 7 days from opening liquidation | podatki.gov.pl – liquidation |

| Summoning creditors in MSiG | Deadline for reporting claims min. 3 months | Art. 279 Code of Commercial Companies |

| Division of assets among shareholders | Not earlier than 6 months from announcement in MSiG | Art. 286 § 1 Code of Commercial Companies |

| Application for removal from KRS | After completion of liquidation and approval of the report | biznes.gov.pl – company liquidation |

What does it look like in practice? Progress Holding experience

In practice, the liquidation of a limited liability company rarely proceeds “by the book”, especially when shareholders or management board members are foreigners. Different jurisdictions, languages, and time zones cause additional risks and delays.

Most common problems we see with our clients

Based on the analysis of over 200 liquidation processes we have conducted at Progress Holding, we see recurring errors. The first is a lack of consistency between shareholders’ resolutions, the articles of association, and KRS entries.

The second common error is omitting the CRBR and NIP-8 update when opening liquidation. The third is planning the division of assets too early, without considering the six-month period from the announcement in MSiG and without fully securing creditors.

Specifics of liquidating companies with foreign participation

With foreigners, signing documents and communicating with courts and offices can be problematic. Sworn translations of powers of attorney, registration documents, or identity confirmations are often needed.

At Progress Holding, we standardly coordinate cooperation with notaries and sworn translators. We prepare bilingual drafts of resolutions and electronic signature instructions so that shareholders can approve documents remotely, e.g., from Germany, Norway, or the United Arab Emirates.

What support do we offer in the liquidation process?

For clients planning the liquidation of a limited liability company, we prepare an action schedule and a list of documents. We keep the company’s accounts during the liquidation period, including preparing the opening balance sheet of liquidation and the liquidation report.

We prepare applications to the KRS in PRS, reports to CRBR, NIP-8, VAT-Z, and ZUS documents. If you plan to close the company in 2026 and want to minimize the risk of errors, contact Progress Holding – we can take over most formalities from you.

Frequently asked questions

Can I close a limited liability company without liquidation?

In Polish law, liquidation of the company before its removal from the KRS is the standard. There are exceptional modes, such as the takeover of company assets by a shareholder or merger, but they require a separate, complex procedure and tax analysis.

Can I be a liquidator of a limited liability company as a foreigner?

Yes, regulations do not forbid foreigners from serving as a liquidator. However, you must be able to submit a qualified signature, trusted profile, or personal signature and effectively communicate with Polish offices. At Progress Holding, we help select a practical representation model involving local managers.

Can a company in liquidation still issue invoices?

Yes, if it is necessary to conclude current company affairs. The liquidator can only conclude contracts that serve to end operations, not to develop them. All revenues and costs in this period go into the company’s books and are subject to taxation.

What happens to employment contracts during liquidation?

A company in liquidation can terminate employment contracts in accordance with labor law regulations. You must settle salaries, leaves, and severance pay, and then deregister employees from ZUS. This often requires parallel HR and payroll service, which we offer at Progress Holding.

Do I have to update data in CRBR during liquidation?

Yes, a change in the company’s status and changes in bodies may require updating data in CRBR. The obligation to update results from the provisions of the Act on Counteracting Money Laundering and Terrorist Financing. Failure to fulfill the obligation carries high financial penalties.

What taxes will shareholders pay after company liquidation?

Shareholders pay income tax on received assets, in the part exceeding the costs of acquiring shares. As a rule, income from liquidation is treated as income from participation in the profits of legal persons. In practice, it is worth performing an individual tax calculation before dividing assets.

Can I sell the company instead of liquidating it?

Yes, selling shares is an alternative to liquidation, but it does not eliminate the company as an entity. You only change owners. If your goal is to completely end the legal existence of the company, the proper path remains liquidation and removal from the KRS.

Closing a limited liability company in 2026 requires good organization, knowledge of regulations, and keeping deadlines. If you run a company with the participation of foreigners or live outside Poland yourself, practical support becomes a necessity. Do you need professional support? Contact us at Progress Holding at +48 603 232 418 or by email office@progressholding.pl.