International invoicing requires knowledge of Polish VAT regulations, EU rules, and everyday business practice. You must correctly determine the place of taxation, the client’s status, the currency, and the invoice wording. A well-designed invoicing process protects your company from corrections, penalties, and payment blocks.

What are the basic rules of international invoicing in 2026?

International invoicing is based on identifying the place of taxation, the client’s status, and the type of transaction. You issue an invoice differently for an EU business and differently for a non-EU consumer.

When a transaction is international

A transaction is considered international when the supply of goods or services involves entities from different countries. This may include clients from the European Union or outside the EU. It also matters where the goods are delivered or where the service is actually performed.

Difference between selling goods and services

- For goods, the key factor is where they are shipped from and where they go.

- For services, what matters is where the customer is established or where the service is actually carried out.

- These rules affect the VAT rate, invoice content, and reporting in JPK_V7.

Difference between B2B and B2C

- B2B means sales between taxable persons, usually with VAT or VAT-EU numbers.

- B2C means sales to consumers, where different VAT rules and registration thresholds often apply.

- This distinction determines whether you apply reverse charge or charge VAT in Poland.

When does an invoice to an EU client include VAT, and when do you use reverse charge?

For most B2B services in the EU, you apply reverse charge and do not add Polish VAT. For goods, you may apply 0% VAT as an intra-Community supply if statutory conditions are met.

Selling goods to EU businesses (ICS/WDT)

If you ship goods from Poland to a company in another EU country and have its valid VAT-EU number, you can apply 0% VAT. The conditions are actual dispatch from Poland and holding transport evidence. On the invoice, you show both parties’ VAT-EU numbers and include wording indicating an intra-Community supply.

Services for EU taxpayers (B2B)

For most B2B services, the place of taxation is the customer’s country. You do not charge Polish VAT and the buyer accounts for VAT under reverse charge in their jurisdiction. Typical wording is “reverse charge,” and you report the sale as not taxable in Poland.

Sales to EU consumers (B2C)

For B2C sales to EU consumers, rules on the place of supply and the EUR 10,000 distance-sales threshold apply. After exceeding the threshold, you usually account for VAT in the consumer’s country, often via the OSS procedure. Current rules are available at Biznes.gov.pl – VAT on sales to EU consumers.

Example combinations for EU clients

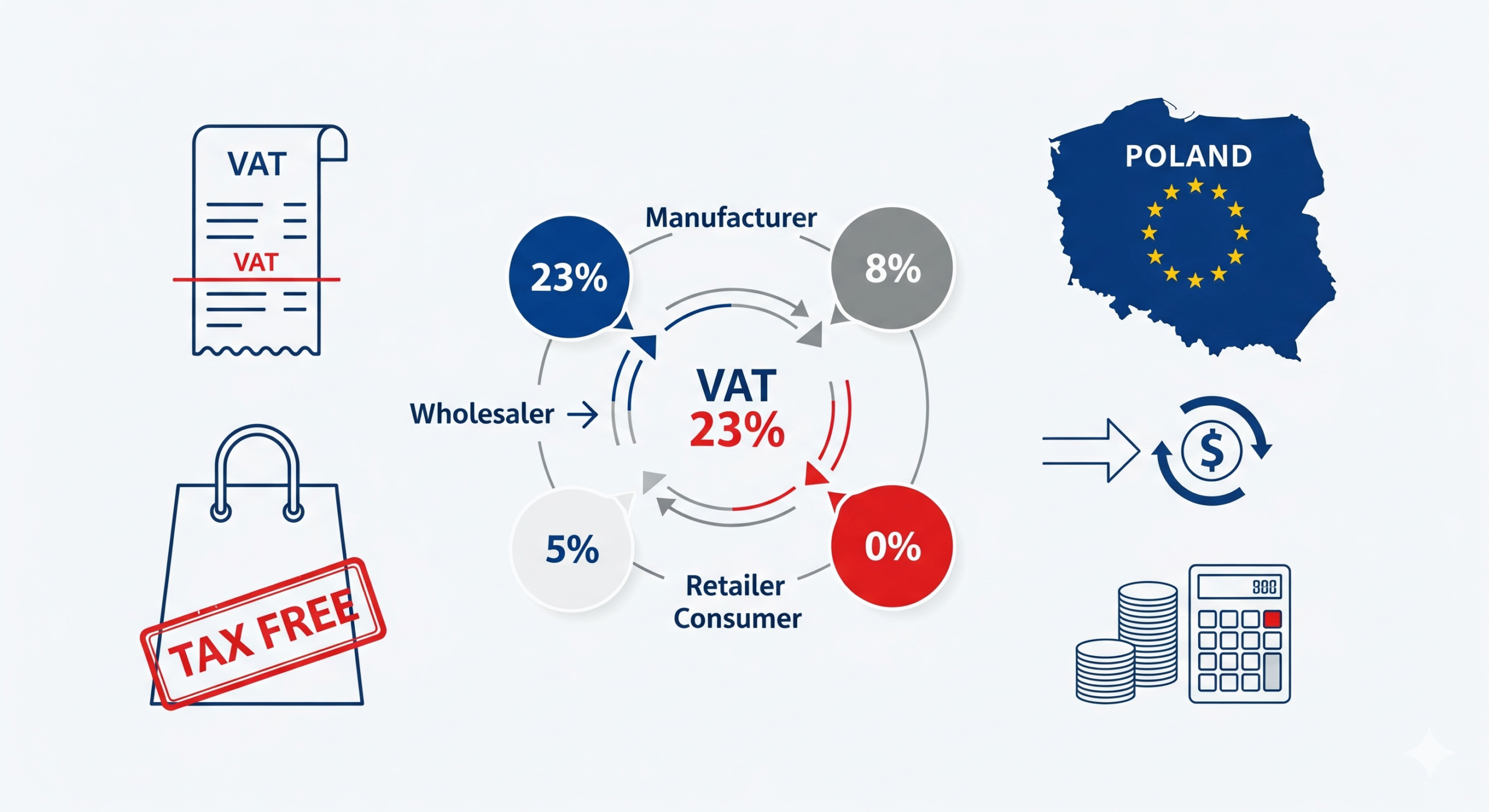

| Type of sale | Client | VAT on invoice | Typical note |

|---|---|---|---|

| Goods (ICS/WDT) | Company with valid VAT-EU | 0% VAT | “Intra-Community supply of goods” |

| B2B services | EU company | No VAT in Poland | “Reverse charge” |

| B2C services | EU consumer | Depends on threshold and OSS | Note aligned with place-of-supply rules |

How to issue an invoice for a client outside the European Union?

For non-EU clients you distinguish between exports of goods and services taxed outside Poland. In both cases, customs documents and correct assessment of Polish VAT applicability are essential.

Export of goods outside the EU

In exports, goods leave the EU customs territory. You may apply 0% VAT if you hold proof of export from the customs system, such as IE-599 messages. The invoice should show the client details, destination country, and indicate that the transaction is an export of goods.

Services for non-EU clients

For B2B services to non-EU entities, the place of taxation is generally the buyer’s country. You do not charge Polish VAT and mark the sale as not taxable in Poland. The buyer settles tax under their local rules.

Typical mistakes on non-EU invoices

- Missing the client’s tax number or using a number that does not meet local requirements.

- Applying the wrong VAT rate on exports due to incomplete customs documentation.

- Confusing exports of goods with logistics services, which follow different VAT rules.

What must an invoice for a foreign client include?

An invoice for a foreign client must comply with the Polish VAT Act. In practice, it is also worth adding items that support international settlements, such as currency, delivery terms, and bank details.

Mandatory elements under the VAT Act

The Polish VAT Act lists the elements required on every invoice. These include the issue date, invoice number, seller and buyer data with identification numbers, as well as a description of goods or services, quantity, unit price, net value, VAT rate and amount, and gross value.

Additional elements for foreign invoices

- Both parties’ VAT-EU numbers or the non-EU client’s local tax number.

- Settlement currency and optionally a separate payment currency.

- Delivery terms, e.g., Incoterms for goods.

- Bank account in IBAN format and SWIFT/BIC code.

- Required notes like “reverse charge,” “ICS/WDT,” or “export of goods.”

Where to check general invoicing rules

Detailed guidance on invoice elements and deadlines is available in the Ministry of Finance explanations at podatki.gov.pl – invoicing rules. The consolidated VAT Act text reflects changes for 2025–2026.

Which currency and exchange rate should you use on an international invoice?

You may issue an invoice in a foreign currency. If you charge Polish VAT, you must convert the taxable base and VAT into PLN using the correct rate.

What currency can be used on invoices

Invoices may be issued in any currency as long as the VAT amount is shown in PLN. For exports or supplies not subject to Polish VAT, the invoice is often entirely in a foreign currency. In practice, EUR and USD are the most common.

Which rate to use for VAT conversion

As a rule, you use the average NBP exchange rate from the last business day before the tax point arises. Alternatively, you may use the ECB rate if applied consistently. The chosen method should be described in your accounting policy and used uniformly.

Most common currency issues on foreign invoices

- Using the wrong date’s exchange rate, creating discrepancies in JPK_V7.

- Failing to show Polish VAT in PLN when VAT is due in Poland.

- Using different rates in accounting and sales systems.

How does KSeF affect international invoicing in 2026?

From 2026, international invoices issued by Polish VAT taxpayers will, as a rule, be sent through KSeF. An exception applies to invoices issued by foreign suppliers who do not have a Polish NIP.

When your foreign invoices will go to KSeF

The largest taxpayers, with sales above PLN 200 million in 2024, will enter KSeF on 1 February 2026. Other entrepreneurs will join on 1 April 2026. This means limited time to prepare your international invoicing procedures in KSeF.

Does every foreign invoice have to be in KSeF?

KSeF covers sales invoices issued by taxpayers with a Polish NIP, including invoices for foreign clients. Purchase invoices from foreign suppliers remain outside KSeF, but must be correctly recorded in your registers and JPK_V7. It is worth checking now whether your invoicing system supports multiple international scenarios in KSeF.

How Progress Holding helps you prepare for KSeF

At Progress Holding we help clients review international invoicing processes and align them with KSeF. We determine which invoice types must go through the system and which remain outside its scope. This allows your company to enter mandatory KSeF without disruption.

How it works in practice: Progress Holding experience

We work with entrepreneurs who sell goods and services across Europe and outside the EU. This gives us insight into where invoicing processes most often get stuck and where tax authorities ask the most questions.

Most common international invoicing errors

- Not verifying the client’s VAT-EU number in VIES before issuing an invoice.

- Applying the wrong VAT rate or misclassifying a transaction as ICS/WDT, export, or a service outside Poland.

- Different client data on the invoice versus the contract or order.

- No consistency between the invoice, transport documents, and customs declaration.

- Incorrect B2B vs B2C classification in online sales.

Support for foreigners running a business in Poland

Many of our clients are foreigners operating in Poland and selling abroad. We help them complete VAT and VAT-EU registration and set up invoicing processes compliant with Polish law. We combine tax advisory with ongoing accounting support to create a safe settlement model.

What a typical cooperation looks like for foreign invoicing

We start by analyzing where you sell, what types of clients you serve, and what contracts you use. Then we design a VAT invoicing and reporting scheme for key transaction types. Finally, we implement it in practice, train your team, and prepare procedures for KSeF entry.

Frequently asked questions

Do invoices for foreign clients have to be issued in Polish?

The law does not require a specific invoice language, but tax authorities may request a Polish translation. For safety, bilingual invoices are often used, especially for larger contracts. What matters most is that the data is clear for both the client and authorities.

Do I always put 0% VAT on invoices for EU businesses?

No. The 0% rate applies, for example, to intra-Community supplies of goods and certain transport services. For most B2B services you use reverse charge and do not show Polish VAT, marking the sale as not taxable in Poland.

How do I verify an EU client’s VAT-EU number before invoicing?

You can verify the VAT-EU number in the VIES online system. Keep a printout or saved confirmation with the transaction documentation. It helps support the 0% rate or reverse charge in an audit.

Do I always have to convert foreign-currency invoices to PLN?

Yes, if Polish VAT is charged, the tax base and VAT must be shown in PLN. The invoice may be in a foreign currency, but VAT calculations require the correct exchange rate. If the sale is not subject to Polish VAT, conversion is mainly for accounting purposes.

Do I have to issue foreign sales invoices in KSeF?

If you are a Polish VAT taxpayer with a PL NIP and issue a sales invoice, you will generally do so in KSeF once the obligation starts in 2026. This also applies to invoices for foreign clients. Purchase invoices from foreign suppliers remain outside KSeF but must be properly booked.

For small online B2C sales to EU customers, do I need VAT registration in every country?

After exceeding the EU EUR 10,000 threshold for B2C distance sales, you can settle VAT via OSS instead of registering separately in each consumer country. This requires correct transaction labeling and reporting.

International invoicing can be set up to be both tax-safe and operationally efficient. If you want to organize your foreign invoices, adapt them to VAT and KSeF, and reduce the risk of disputes with tax authorities, use expert support. Need professional help? Contact us at Progress Holding at +48 603 232 418 or office@progressholding.pl.