What is a fixed asset and when must you depreciate it?

A fixed asset is an asset component that is owned by the company, is complete, fit for use, and you will use it for longer than a year.

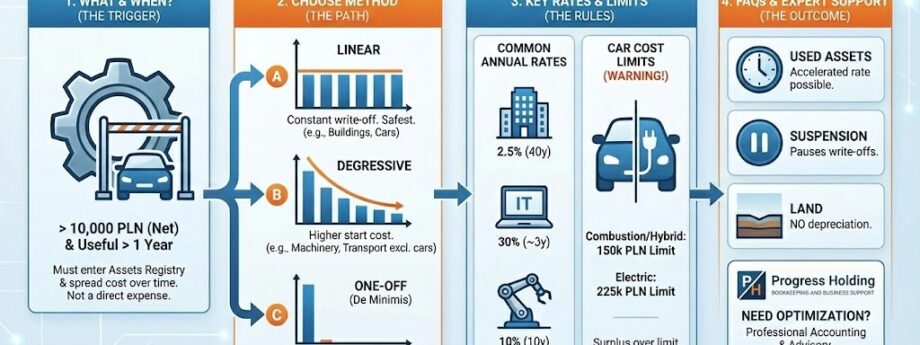

In Polish tax regulations in 2026, the key threshold is the amount of 10,000 PLN net (for VAT payers). If you buy equipment, a machine, or a car worth more than this amount, you cannot put it directly into costs. You must enter it into the fixed assets register and make depreciation write-offs. At Progress Holding, we provide full accounting services, ensuring the correct creation of such records for your company.

Criteria for recognition as a fixed asset:

- Ownership or co-ownership of the taxpayer.

- Completeness and fitness for use on the date of acceptance.

- Anticipated period of use longer than one year.

- Utilization for purposes related to the conducted business activity.

What depreciation methods are available in 2026?

Polish tax law provides for three main depreciation methods: linear, degressive (reducing balance), and one-off (immediate).

The choice of method affects how quickly you “recover” the invested money in the form of tax savings. You make the decision once for a given fixed asset and cannot change it during the write-off period. Our experts at Progress Holding always analyze the client’s financial situation to select the most favorable model.

| Method | Characteristics | For whom? |

|---|---|---|

| Linear | Fixed write-off amount throughout the period. Safest and most common. | Most companies, buildings, passenger cars. |

| Degressive | Higher costs at the beginning, lower in subsequent years. | Machinery and equipment (groups 3-6 and 8 KŚT), means of transport (excluding passenger cars). |

| One-off | The entire value enters the cost in the month of acceptance for use. | Small taxpayers, new companies, fixed assets up to 10,000 PLN. |

What is one-off depreciation (de minimis aid)?

One-off depreciation under de minimis aid allows small taxpayers to include 100% of the value of a fixed asset in costs in the first year of use.

The limit for this relief is the equivalent of 50,000 EUR per year. This applies to brand new as well as used fixed assets classified in groups 3-8 of the Classification of Fixed Assets (KŚT). Passenger cars are excluded from this privilege. This is an excellent solution if you want to quickly reduce high income tax in a given year. Contact us to check if your company meets the “small taxpayer” status.

What are the depreciation rates for popular assets?

The rates result from the List of Depreciation Rates, which is linked to the Classification of Fixed Assets (KŚT).

You cannot set rates arbitrarily. You must assign your equipment to the appropriate KŚT code. Incorrect classification is a risk of costs being questioned by the Tax Office. Below I present typical annual rates:

- Non-residential buildings: 2.5% (depreciation period 40 years).

- Passenger cars: 20% (depreciation period 5 years).

- Computers and IT equipment: 30% (depreciation period 3 years and 4 months).

- Machinery and general-purpose equipment: 10% (depreciation period 10 years).

You can find the full classification list in the regulations available on the ISAP – Internet System of Legal Acts website.

Our data: Common mistakes in car depreciation

Based on the analysis of accounting books of over 150 companies that we transferred to Progress Holding in the last year, we notice one recurring problem. Entrepreneurs constantly ignore depreciation limits for passenger cars.

In 2026, cost limits still apply:

- 150,000 PLN – for internal combustion and hybrid cars.

- 225,000 PLN – for electric cars.

Many foreign investors assume that the operating lease of a luxury car constitutes a tax cost in full. This is a mistake. The surplus over the limit is not a tax-deductible cost (KUP). Our team corrects such errors at the implementation stage, which protects the board from fiscal penal liability.

Frequently Asked Questions (FAQ)

Can I depreciate a used fixed asset?

Yes. If you buy a used fixed asset (used by the previous owner for at least 6 months), you can apply an individual depreciation rate. This allows for shortening the depreciation period, e.g., for a used car to 2.5 years (40% rate).

What if I suspend business activity?

During the period of business suspension, you do not make depreciation write-offs. Asset components are not used in the company then. You resume depreciation from the month following the resumption of activity.

Are lands subject to depreciation?

No, land and the right of perpetual usufruct of land are not subject to depreciation. Their value does not decrease over time (for tax purposes), so they do not generate monthly costs in the form of write-offs.

A correct depreciation strategy is one of the pillars of a safe and profitable business in Poland. Errors in records can cost thousands of zlotys in back taxes. Trust experts who know the regulations inside out.

Do you need professional support in company accounting? Contact us at Progress Holding at +48 603 232 418 or via email at office@progressholding.pl.