Why Registering a Company in Poland as a Non-Resident Can Be a Smart Move

Poland, as a member of the European Union, offers an attractive business environment, especially for non-residents. Companies registered in Poland by foreigners enjoy a number of advantages but also face certain challenges. Let’s examine why company registration in Poland can be a smart move, weighing all the pros and cons.

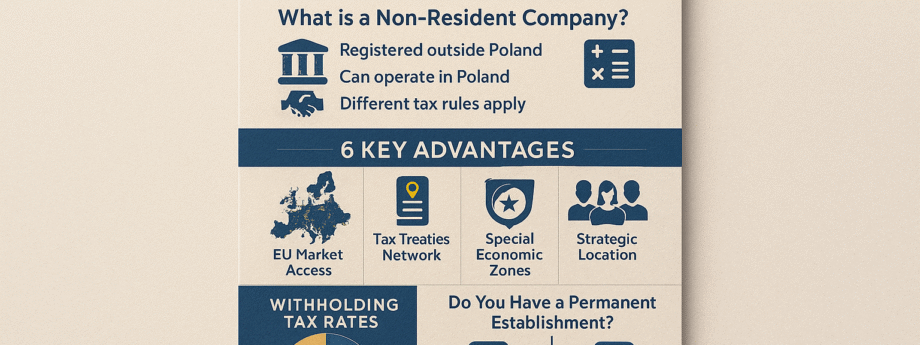

What is a Non-Resident Company in Poland

In Poland, a non-resident company is a company not registered in the territory of Poland. This means that its legal address, place of registration, and typically its main activities are located outside Poland. Regardless of where its head office or main place of business is located, the key factor is the absence of Polish registration.

A non-resident company can conduct economic activities in Poland, but its taxation and legal status are governed by different rules than those for Polish residents. This may include specific requirements for profit taxation, VAT and other taxes, as well as peculiarities of accounting and reporting.

It is important to note that simply having a representative office or branch in Poland does not make a company a resident. Residency is determined by the place of registration of the legal entity.

What Benefits Do Non-Resident Companies Have in Poland

1. Tax Benefits

(It is important to note that tax legislation is constantly changing, and consultation with a tax advisor is necessary)

Tax Treaties

Poland has a network of tax treaties with many countries that can reduce or eliminate double taxation of income earned in Poland. This is particularly beneficial for companies that generate profits from various sources.

Special Economic Zones (SEZ)

Companies located in SEZ may qualify for tax incentives such as reduced corporate income tax rates or exemption from certain taxes. However, the conditions for obtaining these benefits are strict and require meeting specific criteria.

Possibility of Applying Special Tax Regimes

Depending on the type of activity, a company may take advantage of simplified forms of taxation, for example, a simplified taxation system for micro-enterprises (e.g., karta podatkowa – tax card). However, these regimes have limitations on revenue volume and number of employees.

2. Other Non-Tax Related Benefits

Access to the EU Market

Poland is a member of the European Union, which gives non-resident companies access to the vast EU market with its free movement of goods, services, and capital.

Qualified Workforce

Poland has a relatively well-educated and comparatively inexpensive workforce, which can be attractive to many companies.

Geographic Location

Poland’s strategic location in Central Europe provides easy access to other markets in the region.

Developed Infrastructure

Poland has a developed infrastructure, including transportation routes and communication networks.

Stable Political and Economic Situation

Compared to some other countries, Poland offers a relatively stable political and economic environment.

However, there are also disadvantages:

- Administrative burden. Doing business in Poland can involve a significant administrative burden related to compliance with Polish legislation.

- Language barrier. Knowledge of Polish may be necessary for effective business operations.

- Differences in business culture. Differences in business culture may require adaptation and understanding of Polish business practices.

Taxation of Non-Resident Companies in Poland

Taxation of non-resident companies in Poland depends on the type of activity and sources of income. In general, it is regulated by the Corporate Income Tax (CIT) law and other acts. Key aspects:

1. Place of Business:

Permanent Establishment (PE)

If a non-resident company has a permanent establishment in Poland (e.g., office, branch, construction site), the profit obtained through this establishment is taxed in Poland. The definition of permanent establishment is quite complex and depends on the actual circumstances. Even a temporary presence can qualify as a PE if it is sufficiently substantial and prolonged. Tax is calculated on the profit attributable to the PE using the profit allocation method.

Without Permanent Establishment

If a non-resident company does not have a PE in Poland, taxation depends on the type of income received. In this case, the rules for taxation of income sources obtained outside Poland apply.

2. Types of Income and Tax Rates:

Income from Polish Sources

Profit obtained from activities in Poland without a PE may be subject to Polish withholding tax, for example:

- Dividends. Subject to withholding tax (usually 19%, but may be reduced based on double taxation agreements – DTA).

- Interest. Subject to withholding tax (usually 20%, but may be reduced based on DTA).

- Royalties. Subject to withholding tax (usually 20%, but may be reduced based on DTA).

- Other types of income. Depending on the specifics of the income, different rates and taxation methods may apply.

Income from Sources Outside Poland

Income obtained outside Poland is not taxed in Poland if the company does not have a PE in Poland.

3. Double Taxation Agreements (DTA):

Poland has many DTA agreements with other countries. These agreements define rules that prevent double taxation of non-resident company income obtained both in Poland and in the country of residence. They often establish lower withholding tax rates than the standard rates indicated above.

4. VAT:

Non-resident companies may be required to register as VAT payers in Poland if they supply goods or services in the territory of Poland. Registration rules depend on the turnover amount and type of activity.

5. Other Taxes:

Depending on the specifics of the non-resident company’s activities, other taxes may apply, such as excise duties or other local taxes.

IMPORTANT! Polish tax law is complex and constantly changing. To accurately determine the tax obligations of a non-resident company in Poland, it is recommended to consult with a qualified tax advisor or lawyer specializing in Polish tax law. They will help correctly interpret the laws and take into account all specific aspects of your company’s activities.

Conclusion

Overall, the benefits of doing business in Poland for a non-resident company depend on specific circumstances. A thorough analysis of all factors, including tax implications, administrative costs, and market opportunities, is necessary before making a decision. Consultation with lawyers and tax advisors specializing in Polish law is highly recommended.

Company registration in Poland as a non-resident can be a beneficial solution for businesses seeking to expand their presence in the EU market.

If you have any questions, please contact us at office@progressholding.pl