Increasing the share capital of a Polish LLC (spółka z o.o.) is a legal and financial operation that involves raising the total value of contributions made by shareholders. It requires passing a resolution, contributing new funds, paying a 0.5% civil law transactions tax (PCC), and registering the changes in the National Court Register (KRS). This operation effectively boosts the financial credibility of your enterprise.

When is it worth increasing the share capital of a Polish company?

Increasing the share capital is highly recommended before applying for a large corporate loan, entering a public tender, or aiming to improve the company’s image in the eyes of strategic contractors.

The minimum share capital for a limited liability company in Poland is only 5,000 PLN. This amount is often insufficient to commence serious business operations or build market trust. Based on our experience at Progress Holding, banks and financial institutions rigorously analyze the share capital level. High capital sends a strong signal of stability. Your company clearly communicates that it has solid economic foundations and protects its creditors.

Credibility in the eyes of new contractors

Domestic and foreign business partners regularly verify the KRS extract before signing any contract. A contractor is more likely to collaborate with an entity holding a capital of 100,000 PLN rather than one with the absolute minimum. A higher amount guarantees that the company possesses real assets. This significantly increases your negotiating power when determining payment terms.

Better position for bank financing

An increased share capital makes it much easier to obtain leasing for specialized machinery or a corporate vehicle fleet. Many public tenders have strict financial capacity requirements for bidders. A company with adequately high capital easily meets these rigorous criteria. As a result, you bypass formal entry barriers to large infrastructure projects.

What are the ways to increase the share capital in a Polish LLC?

The share capital of a Polish LLC can be increased using external resources through cash and in-kind contributions, as well as using the company’s internal funds, namely from previously retained earnings.

Cash contributions to the company

The most transparent solution is depositing cash directly into the corporate bank account. Existing or entirely new shareholders take up new shares and pay the equivalent of their price as determined in the resolution. This method instantly improves your company’s financial liquidity and provides working capital for daily operations.

In-kind contributions (non-cash assets)

A shareholder can also contribute specific assets of measurable economic value to the company. This could be commercial real estate, production machinery, proprietary software, or a heavy-duty vehicle. At Progress Holding, we often notice that valuing in-kind contributions made by foreigners requires preparing additional sworn translations and external asset valuation documents.

Increasing capital directly from company profits

Your company can utilize surplus funds previously accumulated as supplementary or reserve capital. These must come from a properly approved net profit from previous years. In this scenario, shareholders do not pay new money out of pocket. It is simply an accounting structural shift within the company’s balance sheet liabilities. This increases the formal share capital without draining the shareholders’ wallets.

How does the procedure for changing the articles of association work?

The procedure for amending the articles of association to increase capital requires a notarial deed, submission of declarations on taking up shares, contribution of funds, and a correct application to the KRS.

Step 1: Passing a resolution of the shareholders’ meeting before a notary

The process always begins with convening an extraordinary shareholders’ meeting. Shareholders vote on a resolution to amend the articles of association. The resolution must precisely specify the increase amount and the type of contributions made. The Polish Commercial Companies Code requires a 2/3 majority vote here. Since the text of the agreement itself changes, a visit to a notary who will draft the appropriate protocol is absolutely mandatory.

Step 2: Declarations of taking up new shares

After the main resolution is passed, shareholders must submit formal declarations. Each shareholder individually declares how many new shares they are taking up and exactly how they will pay for them. These declarations strictly require the form of a notarial deed. At the Progress Holding office, we continuously assist in preparing complete, error-free documentation for the notary’s office.

Step 3: Covering the increased capital by shareholders

Shareholders have an absolute obligation to make the declared contributions. Cash funds must physically reach the corporate account before submitting the application. The company’s management board must submit a written statement declaring that all contributions for the increased capital have been fully made. The properly signed board statement is then attached to the documentation for the commercial court.

Step 4: Application to the National Court Register (KRS)

The management board reports the formal change to the registry court via the IT system called the Court Registers Portal (PRS). We have conducted hundreds of such processes and know that technical errors in applications are the most common cause of painful document rejections by the court. A complete application must include necessary attachments. These include: the notarial resolution, shareholders’ declarations, an updated list of shareholders, and proof of court fee payment.

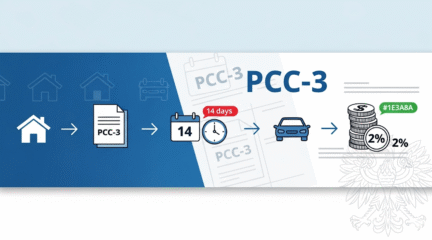

Step 5: Timely payment of PCC tax to the tax office

The company is obliged to submit a PCC-3 declaration to the competent tax office. The due tax must be paid within a strict deadline of 14 days from the date the resolution was passed. The tax is calculated exclusively on the capital increase amount itself. This tax base can be legally reduced by documented notarial and court fees.

What are the costs of increasing the share capital in 2026?

The costs of increasing the share capital in 2026 include a fixed court fee for the KRS (250 PLN), a PCC tax of 0.5% of the increase amount, and a notarial fee set according to regulations.

When deciding on a recapitalization operation, your company must prepare a suitable budget for formalities. Legal regulations from late 2025 slightly reduced the total bureaucratic burden. The government removed the obligation to publish announcements in the Court and Economic Monitor (MSiG). This change saves exactly 100 PLN on every single application submitted to the KRS.

Summary of basic administrative and legal fees

The table below presents the main categories of expenses you will encounter during the entire process. The table will help you safely estimate the costs for your business.

| Type of cost / Fee | Applicable rate in 2026 | Legal basis and additional notes |

|---|---|---|

| Court fee (KRS application via PRS portal) | 250 PLN | Art. 55 of the Court Costs Act. From 2025, no MSiG publication fee. |

| Court fee (S24 IT system) | 200 PLN | Available only to companies whose agreement was never amended before a notary. |

| Civil law transactions tax (PCC-3) | 0.5% of the increase amount | Paid within 14 days. The tax base is reduced by notary and KRS costs. |

| Notary fee (notarial deed service) | Depends on the increase amount | The rate grows with the amount. E.g., for a 100,000 PLN increase, the fee is approx. 1,000 PLN net. |

| Legal assistance / Full KRS change service | From 1,500 PLN net | Standard price at Progress Holding for remote KRS data update – completely without the client’s presence. |

If the company’s share capital grows by 100,000 PLN, the PCC tax alone is approximately 500 PLN. You can reduce the final tax value by deducting the notary fee and the court fee paid via the PRS system.

How to increase the capital using the S24 system?

Increasing the capital in the S24 system is available only to companies registered through this government portal, provided their articles of association have never been modified before a notary.

In the S24 system, the entire process takes place completely online. Shareholders log into the Ministry of Justice portal and approve resolutions using a Trusted Profile (Profil Zaufany) or a qualified electronic signature. This allows you to avoid notary service costs. The court fee for the KRS is a discounted 200 PLN instead of the standard 250 PLN. Nevertheless, the obligation to submit a paper or electronic PCC-3 declaration still applies to your company without exception.

What are the tax consequences for shareholders after a capital increase?

Increasing the company’s capital does not trigger income tax for the shareholder upon a cash deposit, but it does create a tax liability when the contribution is an in-kind asset valued above its market value.

No income tax upon cash deposit

Simply making a cash contribution to cover new shares in an LLC is completely neutral regarding PIT and CIT income taxes. The money invested in the company does not constitute taxable income for you. The Tax Office treats this capital movement merely as a natural asset transfer. The shareholder will only pay tax if they sell their shares in the future for more than they originally acquired them.

Taxation of in-kind contributions made to a Polish company

The situation gets complicated when making non-cash contributions. Taking up shares in exchange for an in-kind contribution constitutes income for the shareholder. This income is equal to the market value of the contributed asset. If the valuation of the machinery or software significantly exceeds its historical acquisition costs, the shareholder will pay income tax on the resulting difference. The valuation of the contribution must always reflect actual market realities. The tax authority strictly controls such economic operations.

How does it look in practice? Progress Holding’s experience

Based on our analysis of over 500 corporate change processes conducted at Progress Holding, the most common mistake made by entrepreneurs is being late with submitting the PCC-3 declaration and waiting too long for the shareholders to transfer the funds.

Many foreigners successfully register companies in Poland. However, lacking a Polish PESEL number can be a major obstacle during notarial procedures and account authentication in the PRS system. We offer clients efficient assistance in obtaining PESEL numbers for foreign board members. It frequently happens that paper declarations on taking up shares are signed outside Poland. In such cases, Polish courts absolutely require an apostille clause and the seal of a sworn translator into Polish.

Another practical issue is the correct accounting classification of the made contributions. Shareholders regularly execute bank transfers with very imprecise payment titles. We always recommend titling such transfers strictly according to the following template: “Payment to cover new shares in the increased share capital, resolution dated [date]”. We provide professional accounting for foreigners; our company accounting services start from 799 PLN net. We strictly supervise the proper document flow for all our clients to avoid penalties from tax offices.

When to submit the application to the KRS after passing the notarial resolution?

The management board of an LLC must report the formal share capital increase to the National Court Register within a strict deadline of 6 months from the date of passing the relevant resolution.

Ignoring this important deadline has severe and costly consequences for the business. After the strict 6 months expire, the shareholders’ resolution automatically loses its legal force. The registry court will officially dismiss the late application filed by the board. The money previously transferred to the corporate account suddenly becomes an undue benefit in the eyes of the law. The company is obliged to return it to the shareholders immediately. The entire burdensome procedure, including notary fees, must then be irrevocably repeated from the very beginning.

What are the alternatives to increasing the share capital?

The most popular alternatives to increasing the share capital in Poland are direct shareholder surcharges (dopłaty) to the company and securely granting a cash loan to the company by a shareholder.

Shareholder surcharges to the company

Voting for surcharges is a mechanism that guarantees the company a quick cash injection without the need to visit a notary. However, the articles of association must stipulate such a possibility for the shareholders in advance. The collected surcharges increase the internal reserve capital, not the statutory capital in the KRS. They are subject to PCC tax at a rate of 0.5%. In the future, upon good financial results, they can be easily returned to the shareholders without triggering the complicated share redemption procedure.

Private loan from a main shareholder

A shareholder owning even a fraction of shares in a capital company can legally grant it a private loan. The main advantage of this rapid solution is complete exemption from PCC tax under current legislation. The interest paid to the shareholder constitutes a tax-deductible expense for the company itself. This is an extremely popular method of recapitalizing entities during their difficult first years of operation on the Polish market.

Frequently asked questions

How much is the PCC tax on a capital increase?

The civil law transactions tax (PCC) is exactly 0.5% of the net value by which the total share capital of the LLC is increased. According to tax office guidelines, before the final calculation, the tax base is reduced by the notarial and court fees collected in connection with the entire registration.

Are the KRS fee and notary fee always required?

Yes, any interference with the size of the share capital absolutely requires a court fee to the Polish KRS. In turn, a notary is mandatory when the entire operation requires modifying the original text of the articles of association. However, in the S24 mode, you can efficiently avoid visiting the law office, provided that the e-agreement has never been touched by a notary before.

Can a foreigner easily take up new shares in a Polish company?

Yes, a foreign investor freely takes up newly issued shares in Polish companies. An important exception is when the subject of an in-kind contribution from abroad is agricultural real estate or the foreigner gains absolute control over a company that owns land in Poland. Such a move requires prior approval from the Polish Minister of the Interior and Administration.

Can the company use the deposited funds before registration in the KRS?

Yes, the management board of a Polish LLC has the full right to use the financial funds deposited by investors before the judge approves the case in the KRS. The deposited money becomes the natural property of the enterprise from the second it is credited to the bank account. You can legally use it to pay current invoices or salaries.

Who personally signs the application to the KRS for capital changes?

The application to the registry court for the formal entry of a capital increase is always approved by the incumbent management board of the limited liability company. The complete form in the government PRS system must be signed in accordance with the binding rules of representation. Commercial qualified electronic signatures or free Trusted Profiles of board members are used for this purpose.

Summary

Increasing the share capital is a strategic investment that instantly opens doors to conquering foreign markets, securing high investment loans, and winning profitable state tenders. The procedure always requires strict compliance with notarial requirements and perfect submissions in the KRS IT systems. Reliable substantive support from advisors minimizes the burdensome risk of document rejection by the judge. Do you need professional support in making changes to your company? Contact us at Progress Holding by calling +48 603 232 418 or emailing office@progressholding.pl.