If your company is registered in Poland, you must file the annual CIT-8 return electronically by 31 March 2026. Corporate income tax (CIT) must also be paid by the same date. The current form version is CIT-8(34). Below you will find a complete overview of deadlines, required documents, and errors to avoid.

What is the CIT-8 return and who must file it?

CIT-8 is the annual corporate income tax return in Poland. It reports the taxable income or loss of a CIT taxpayer for the given tax year. Every CIT taxpayer must file this return — regardless of financial results.

Entities required to file include: limited liability companies (sp. z o.o.), joint-stock companies (S.A.), cooperatives, foundations, associations, and companies in organisation. The obligation exists even if the company had no revenue, incurred a loss, or was dormant throughout the year.

A common misconception among foreign business owners in Poland is that a dormant company with no turnover does not need to file CIT-8. This is incorrect — failure to file may result in criminal fiscal liability under Polish law.

Who is exempt from CIT-8?

Exemptions apply to entities listed in Article 6(1) of the Polish Corporate Income Tax Act — including the State Treasury, the National Bank of Poland, and certain investment funds. A standard sp. z o.o. always files CIT-8.

When is the CIT-8 filing deadline for 2025?

The CIT-8 return for the 2025 tax year must be filed by 31 March 2026 — for taxpayers whose tax year coincides with the calendar year. Tax payment or the balance between tax due and advance payments made during the year is also due on this date.

If your company has a non-calendar tax year, the deadline is the end of the third month following the close of that year. Legal basis: Article 27(1) of the CIT Act.

Key compliance dates — CIT-8 and financial statements for 2025

| Obligation | Deadline | Notes |

|---|---|---|

| Preparation of financial statements | 31 March 2026 | 3 months from the balance sheet date |

| CIT-8 filing and tax payment | 31 March 2026 | Form CIT-8(34), electronic only |

| Approval of financial statements | 30 June 2026 | 6 months from the balance sheet date |

| Submission of statements to KRS (court register) | 15 July 2026 | 15 days from approval |

| JPK_KR_PD (revenue >EUR 50m or tax groups) | 31 July 2026* | *Proposed extension from 31 March to 31 July |

Source: Polish Ministry of Finance — gov.pl

What documents do you need to file CIT-8?

Filing CIT-8 correctly requires a complete set of accounting records for the entire tax year. The return itself is an electronic form, but behind it lies your company’s full-year bookkeeping.

Source documents checklist

- Accounting books — a full record of all business transactions maintained in accordance with the Polish Accounting Act.

- Financial statements — balance sheet, profit and loss account, and supplementary notes. These must be prepared in XML format (e-Sprawozdanie).

- Fixed asset register — including up-to-date depreciation schedules.

- VAT records — sales and purchase registers for the full year (JPK_V7M or JPK_V7K files).

- Bank statements — confirming CIT advance payments made during the year.

- Cost documentation — invoices, receipts, and contracts supporting tax-deductible expenses.

- Transfer pricing documentation — required if you carry out transactions with related parties above statutory thresholds.

- UPL-1 power of attorney — if the CIT-8 is signed and submitted by an accountant or accounting firm on the company’s behalf.

Attachments to the CIT-8(34) form

You only attach the schedules that apply to your situation. Do not submit blank forms. The most commonly used attachments are:

- CIT-8/O(20) — information on deductions from income and tax, and tax-exempt income. Required when claiming reliefs or exemptions.

- CIT-D — information on donations received or made.

- CIT/M(1) — minimum tax information. Required if your company reports a loss or income below 2% of revenue.

- CIT-ST — information on the taxpayer’s branches, filed when the company has establishments in different municipalities.

- CIT/WOT(1) — a new form introduced for 2025, covering deductions for employing members of Poland’s Territorial Defence Forces or Active Reserve.

- CIT/8S and CIT/8SP — information on activities in special economic zones or under investment support decisions.

The full list of CIT forms is available at: podatki.gov.pl/cit/formularze-do-druku-cit.

How to file CIT-8 electronically

CIT-8 for 2025 must be filed exclusively in electronic form. Two channels are available: the e-Deklaracje gateway (using a qualified electronic signature) or the e-Urząd Skarbowy portal (using a trusted profile, online banking, mObywatel app, or e-Dowód).

Before submission, make sure the person signing the return has a valid UPL-1 power of attorney registered with the tax office. Without it, your accounting firm cannot sign the CIT-8 on your company’s behalf.

From our experience at Progress Holding, the most common technical issue during submission is an expired qualified signature or a missing UPL-1 filing. We always verify these well in advance to avoid last-minute problems.

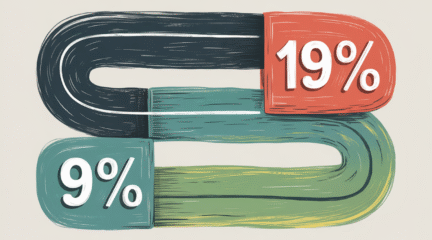

CIT tax rates in Poland for 2025

| CIT rate | Condition |

|---|---|

| 9% | Small taxpayers (revenue up to EUR 2 million) — on operating income only (not capital gains) |

| 19% | All other taxpayers and income from capital gains |

| 10% (minimum tax) | Taxpayers with a loss or income below 2% of revenue (with exclusions) |

Legal basis: Article 19 of the Act of 15 February 1992 on Corporate Income Tax (Journal of Laws 1992 No. 21 item 86, as amended).

What is the minimum tax and does it apply to your company?

The minimum tax is a levy of 10% on a specific tax base, applicable to CIT taxpayers that report a tax loss or income below 2% of revenue (excluding capital gains). It was first applied for the 2024 tax year and continues on the same terms for 2025.

The minimum tax is reported in field 258 of the CIT-8(34) form, and you must complete the CIT/M(1) attachment. However, check whether your company qualifies for an exclusion.

Who is excluded from the minimum tax?

- Small CIT taxpayers (revenue up to EUR 2 million).

- Companies in their first 3 years of operation.

- Entities whose revenue declined by at least 30% year-on-year.

- Companies that achieved profitability of 2% or more in at least one of the last three tax years.

Most common mistakes in CIT-8 returns

Errors in your CIT-8 return may lead to tax arrears, interest charges, and criminal fiscal liability. Below are 6 of the most frequent mistakes we encounter at Progress Holding.

1. Incorrect classification of tax-deductible costs

A frequent issue is claiming expenses that do not meet the definition under Article 15(1) of the CIT Act. This includes entertainment expenses, contractual penalties for late performance, and interest on liabilities paid after the due date.

2. Missing or incorrect CIT-8/O attachment

If your company claims reliefs (e.g. R&D relief, IP Box) or exemptions, you must complete the CIT-8/O form. Omitting this attachment means losing the right to the deduction.

3. Errors in loss carryforward

Tax losses from previous years can be carried forward for a maximum of 5 consecutive tax years. In any single year, you may deduct no more than 50% of the total loss. Exceeding these limits is a common error.

4. Discrepancies between JPK_V7 data and CIT-8

Revenue and cost figures in CIT-8 must be consistent with the data reported in JPK_V7 filings throughout the year. Discrepancies trigger immediate attention from the tax authorities.

5. Late filing

Filing CIT-8 after 31 March 2026 constitutes a fiscal offence or crime under the Polish Fiscal Penal Code. Fines for a fiscal offence may range from 1/10 to 20 times the minimum wage. In cases of tax evasion, fines of up to 720 daily rates or imprisonment may apply.

6. Overlooking the minimum tax

Since the 2024 tax year, the minimum tax has been mandatory. Companies reporting a loss or low income must check whether they are subject to this tax and correctly complete the CIT/M attachment. Failing to do so results in tax arrears.

JPK_CIT — new reporting obligation from 2025

JPK_CIT (JPK_KR_PD) requires taxpayers to electronically submit their accounting books to the tax office in a structured format. From 1 January 2025, this applies to the largest taxpayers — those with revenue exceeding EUR 50 million and tax capital groups.

The first JPK_KR_PD file for 2025 is submitted alongside the CIT-8 return. A proposed deadline extension (to 31 July 2026) is currently under legislative review. From 1 January 2026, the obligation will extend to the next group of CIT taxpayers — those required to file JPK_V7M.

Having processed hundreds of year-end closings at Progress Holding, we know that preparing for JPK_CIT requires proper chart of accounts mapping and tagging throughout the year. We strongly recommend not leaving this to the last moment.

JPK_CIT implementation timeline

| Tax year starting after | Who is affected | Filing deadline |

|---|---|---|

| 31 December 2024 | Tax capital groups and CIT payers with revenue >EUR 50m | 31 March 2026 (or 31 July 2026*) |

| 31 December 2025 | Other CIT payers filing JPK_V7M | 31 March 2027 |

| 31 December 2026 | All remaining CIT payers | 31 March 2028 |

*Draft law UD350 proposes extending the deadline to the end of the 7th month following the close of the tax year. Source: EY Poland — UD350 draft.

How much does CIT-8 and financial statement preparation cost?

At Progress Holding, professional preparation of the annual financial statements and CIT-8 return starts from PLN 1,500 net. This includes the balance sheet, profit and loss account, supplementary notes, corporate resolutions, and the CIT-8 form with all applicable attachments.

Additional services — such as VAT/CIT return corrections — start from PLN 250 net. Ongoing accounting services for companies begin at PLN 799 net per month. The current price list is available at: progressholding.pl/cennik-uslug.

When you entrust us with full-year accounting, the financial statements and CIT-8 are prepared as part of the engagement — giving you confidence that everything is consistent and filed on time.

What we see in practice — insights from Progress Holding

Based on our analysis of over 500 annual filings processed at Progress Holding in the past three years, we have identified three areas that cause the most problems for our clients.

Most common issues from our data

- 42% of companies that came to us from other accounting firms had discrepancies between their JPK_V7 data and annual CIT-8 return. This was most often caused by differences in cost classification between VAT and CIT.

- One in three companies among new clients did not have a valid UPL-1 power of attorney registered with the tax office — which blocked timely submission of their return.

- Around 15% of companies using the reduced 9% CIT rate did not monitor whether they had exceeded the EUR 2 million gross revenue threshold during the year. Exceeding this threshold means losing the preferential rate for the entire year.

Each of these issues can be eliminated by working with an experienced accounting firm. At Progress Holding, we monitor thresholds and deadlines year-round — not just in March.

Frequently asked questions

Do I have to file CIT-8 if my company had no revenue?

Yes. All CIT taxpayers must file CIT-8, regardless of whether they generated revenue, income, or a loss. Failure to file may result in fines under the Fiscal Penal Code.

Can I file CIT-8 on paper?

As a general rule — no. CIT-8 must be filed electronically with a qualified electronic signature or via the e-Urząd Skarbowy portal. An exception applies only to taxpayers earning exclusively CIT-exempt income who are not required to file PIT returns for employees (Article 27a of the CIT Act).

What are the penalties for late CIT-8 filing?

Late filing is classified as a fiscal offence or crime, depending on the amount of tax shortfall. Fines for a fiscal offence can reach 20 times the minimum wage. For larger amounts, penalties may include fines of up to 720 daily rates or imprisonment.

Can Progress Holding prepare and file CIT-8 for my company?

Yes. Progress Holding prepares the complete annual filing package: financial statements, CIT-8 with all attachments, corporate resolutions, and electronic submission. Prices start from PLN 1,500 net.

What is the difference between CIT-8(33) and CIT-8(34)?

Version CIT-8(33) was used for the 2024 tax year. Version CIT-8(34) applies to tax years beginning after 31 December 2024 — i.e. the standard 2025 filing. The new version reflects changes to attachments (CIT/WOT) and updates to the minimum tax form.

When do I need to file JPK_CIT alongside CIT-8?

For the 2025 tax year, the obligation to submit JPK_KR_PD alongside CIT-8 applies only to tax capital groups and CIT taxpayers with revenue exceeding EUR 50 million. Other taxpayers will be covered in subsequent years.

Filing CIT-8 for 2025 is a process worth planning ahead. Properly maintained accounting records throughout the year are the foundation of a smooth year-end closing. If you have any doubts or need professional support — do not wait until March.

Need help with CIT-8 or financial statements? Contact Progress Holding at +48 603 232 418 or by email at office@progressholding.pl. We serve over 500 companies and have been helping businesses in Poland file their taxes correctly and on time for over 20 years.